India’s largest producer of coking coal, Bharat Coking Coal Ltd (BCCL), is hitting the public markets. As a critical player in steelmaking—providing nearly 60% of India’s domestic coking coal—this IPO has drawn significant interest, already oversubscribed eight times. But before you join the rush, let’s unpack whether this is a golden opportunity or a risky, niche bet.

What Makes Coking Coal Special?

Unlike the thermal coal used in power plants, coking coal is a key ingredient in steel production. It’s baked into coke, which fuels blast furnaces. BCCL operates exclusively in the rich Jharia (Jharkhand) and Raniganj (West Bengal) coalfields. However, Indian coking coal has a catch: high ash content. It must be washed and blended with imported coal, making production more complex.

The IPO & Valuation: A Tale of Two Bases

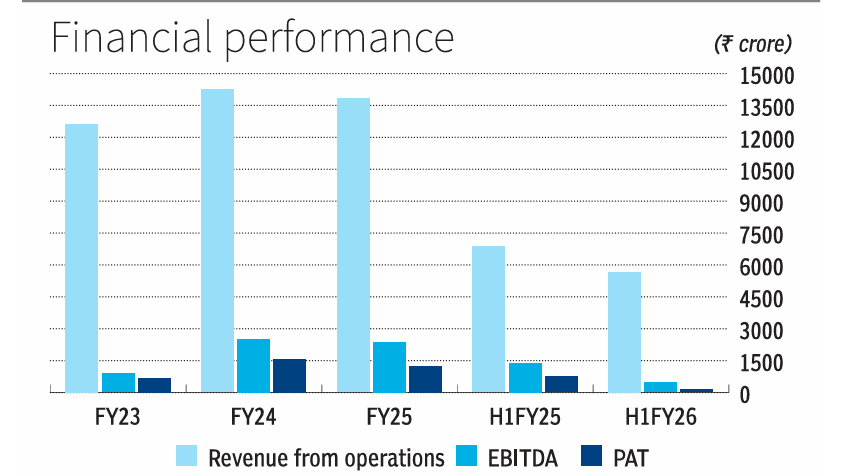

The government is offering 46.57 crore shares at ₹23 apiece, raising ₹1,071 crore for parent Coal India. On the surface, valuations look cheap—at 8.7 times FY25 earnings. But here’s the twist: profits fell 83% year-on-year in the first half of FY26. Using these last twelve months (LTM) figures, the valuation jumps to 17.4 times earnings. This stark difference highlights the cyclical volatility in earnings. Compared to its diversified parent Coal India, which trades at 7.5 times LTM earnings, BCCL looks expensive on a risk-adjusted basis.

Business Mix: More Power, Less Steel

Surprisingly, despite being a coking coal champion, BCCL’s revenue is dominated by the power sector (~74% in FY25). Only about 18% comes from steel. The company is trying to shift this balance by ramping up washed coal capacity for steelmakers, but the transition is ongoing.

Earnings: A Rollercoaster Ride

BCCL’s profits are tightly linked to global coking coal prices. FY24 was a bonanza year post the Russia-Ukraine conflict. Since then, profits have normalized and recently slumped due to softer prices and operational disruptions. Notably, recent reported profits have been propped up by ‘other income’ like interest, not core operations.

Key Risks to Consider

- Cyclical Sensitivity: Earnings swing wildly with global coal prices.

- Operational Hurdles: Heavy exposure to the challenging Jharia field and rising contractor costs squeeze margins.

- Financial Contingencies: Significant contingent liabilities (₹3,599 crore) loom over its balance sheet.

The Big Question: BCCL or Coal India?

This is the core of the investment decision. Coal India is a diversified, cash-generating giant with stable thermal coal margins. BCCL is a concentrated, cyclical bet within the same group. For long-term investors, owning the parent offers broader exposure and less volatility. BCCL’s IPO offers a pure-play on coking coal, but at current pricing, it doesn’t clearly offer a better risk-reward payoff than simply investing in the steadier, already-listed Coal India.

Verdict: Watch, Don’t Leap

While BCCL is strategically important to India’s steel ambitions, the IPO comes at a time of earnings stress and rich valuation compared to its parent. For most long-term investors, there is little compelling reason to choose this volatile, niche subsidiary over the established, diversified giant that is Coal India. It might be prudent to stay on the sidelines for this one.

The IPO closes on January 13.